Sponsored article: Ian Buckle and Rory Sandilands discuss why short-dated corporate bonds which are relatively close to maturity can help investors capture attractive yields with minimal interest-rate sensitivity, low portfolio volatility and good levels of liquidity, and all while having a relatively low carbon footprint.

Short-dated investment-grade bonds can be attractive for a range of clients, including pension schemes undergoing de-risking, insurers, treasurers seeking enhanced returns above cash rates and wealth management clients focused on preserving capital.

The appeal of short-dated investment grade bonds

The unique characteristics of short-dated bonds offer investors an opportunity to access a lower-volatility segment of the broader fixed income market.

They can be attractive to a diverse range of clients, such as treasurers seeking enhanced returns above cash and pension schemes undergoing de-risking.

Their appeal is based on a range of factors:

- A record of generating attractive risk-adjusted returns;

- Capital-preservation qualities; individual bonds are typically much more resilient to negative company-specific events than longer-dated bonds.

- They are less susceptible to fluctuating interest rates, because they derive returns through credit risk rather than duration risk;

- They can generate steady cashflows, which can be paid-out as an income or reinvested to take advantage of further opportunities;

- Short-dated bonds are inherently more liquid than their longer-dated equivalents, due to the relatively high frequency of bonds reaching maturity;

- There is no material cost to having a low carbon footprint.

It is this final benefit that we want to explore in more detail.

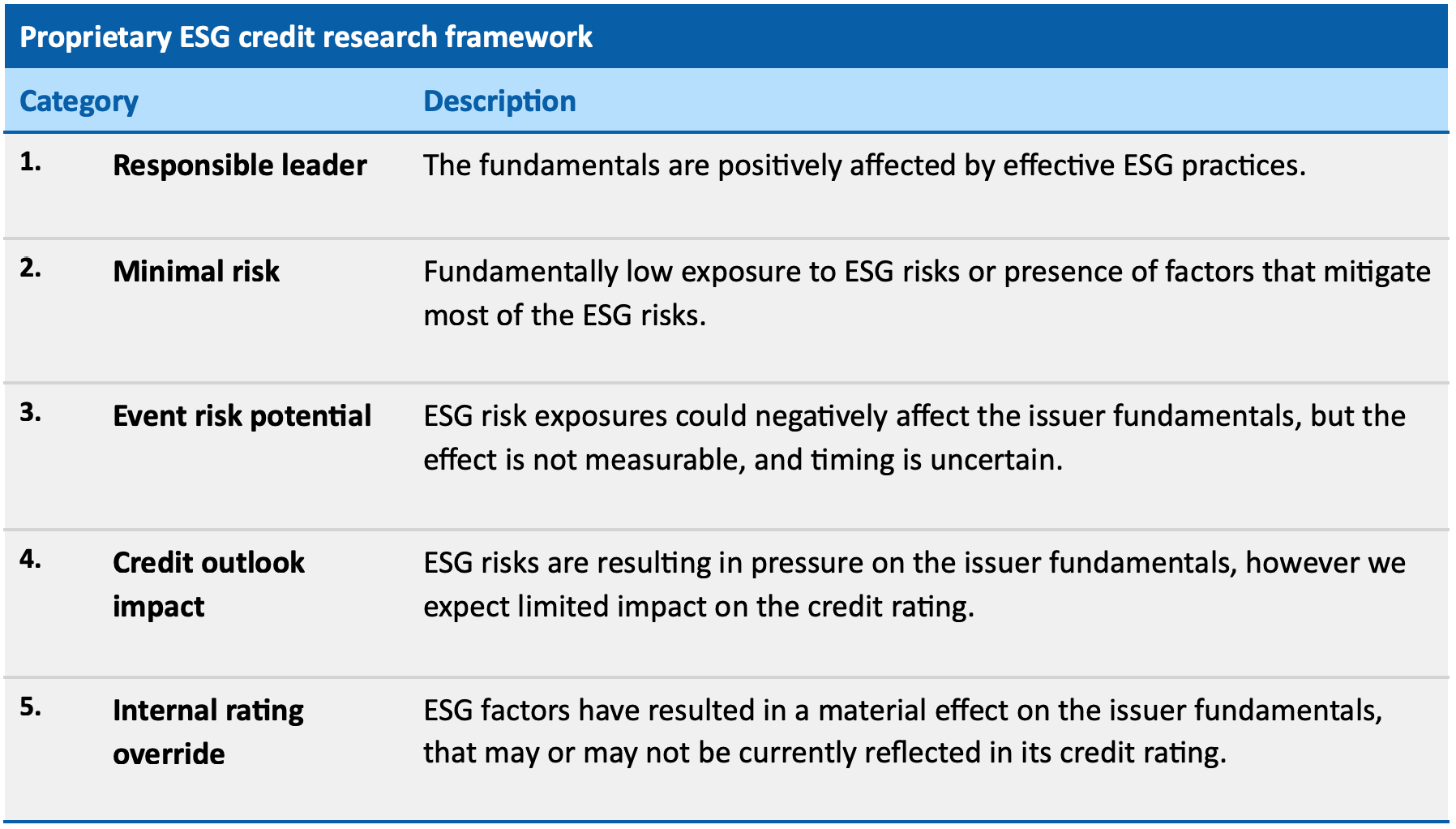

Assessing material ESG issues

When assessing an issuer’s credit profile we utilise a proprietary ESG credit framework based on five categories, as outlined in the table below.

An ESG category is assigned to each issuer based on our determination of the materiality of ESG factors and the impact on an issuer’s credit fundamentals.

climate risk considerations

Within the environmental component of our ESG research, climate-related risks are a particular area of focus, especially in higher-influence sectors such as energy, utilities and transport. However, if you look beyond the headline emission numbers, then other sectors also carry climate risks.

There are challenges to overcome in the banking sector, not least the varying degrees of willingness by the banks themselves to adopt aggressive targets to reduce climate exposures.

The practicalities of reducing carbon intensity for a bank’s loan portfolios are also demanding and it can take many years to effect meaningful change.

As fixed income investors we believe the best way to understand and manage these risks is through active engagement with banks and other financial institutions. This enables us to encourage more aggressive targets and help improve the quality of disclosures from large financial institutions.

Maturity and climate risks

The analysis and decisions made around climate risk can vary significantly, depending on the maturity of an individual bond.

This is because some of the key climate risks in areas such as stranded assets and the costs of transition can take many years to play out.

Although we can potentially identify those risks now, they can take a long time to significantly impact a company’s credit profile. In general, the longer you lend to a company that potentially faces climate risks, the more you are exposed to those risks. So, for holders of longer-dated bonds, especially through buy-and-hold strategies, it is vital to analyse and understand climate change risks.

If you are lending to climate-exposed companies over the longer term, then you can typically get paid a premium for doing so. But this is not true for shorter-dated bonds, which are much less exposed to a climate-related deterioration in credit quality during their lifetime.

What this means is that it is possible to have a short-dated investment grade credit portfolio that does not sacrifice expected return, but which has a weighted average carbon intensity of around two-thirds less than the broader short -investment grade universe. This is potentially attractive to investors as regulatory, societal and investment pressures lead to a greater awareness of climate-related risks.

Ian Buckle is head of credit and Rory Sandilands is fixed income investment manager at Aegon AM.

Photo by Timothy Eberly on Unsplash

—————

FREE monthly newsletters

Subscribe to Room151 Newsletters

Room151 Linkedin Community

Join here

Monthly Online Treasury Briefing

Sign up here with a .gov.uk email address

Room151 Webinars

Visit the Room151 channel