Additional research: Atharva Deshmukh.

As the chancellor delivered his spending review the local government borrowing terrain was rocked by a PWLB rate cut of 100bps despite bond issues showing signs of growing momentum.

Separate developments have this week made local government borrowing contested ground. First the UK Municipal Bonds Agency unveiled its third bond issue bringing the total value up to £850m in a year and marking a distinct turn from PWLB borrowing. But then the chancellor’s spending review saw the Treasury reveal that PWLB would cut all standard and certainty rate loans by 100bps, sending shockwaves into local authority treasury departments across the country.

The developments are likely to prompt a pause in finance departments as officials assess the new borrowing landscape. It was only 12 months ago that PWLB raised loan rates amid concerns about the sums invested in commercial property by councils.

“HM Treasury would not have made this move had it not been for the few public bond market deals proving that was a cheap practical alternative.”—Mike Jensen

According to Mike Jensen, director for investment at Lancashire County Council, which this year sealed more than half a billion in borrowing through UKMBA, the rising popularity of other lending providers has prompted the policy change at PWLB.

“HM Treasury would not have made this move had it not been for the few public bond market deals proving that was a cheap practical alternative,” he says.

This week the UKMBA finalised arrangements for Warrington council to issue the agency’s third bond, this time for £250m, bringing the agency total to £850 (thisincludes two bonds issued by Lancashire CC of £350m and £250). Add in Sutton’s public bond of £250m issued this month and councils have used bonds for more than £1bn in borrowing. The use of a £75m interest rate swap by Plymouth earlier this year indicates local authorities are willing to further diversify their borrowing strategies.

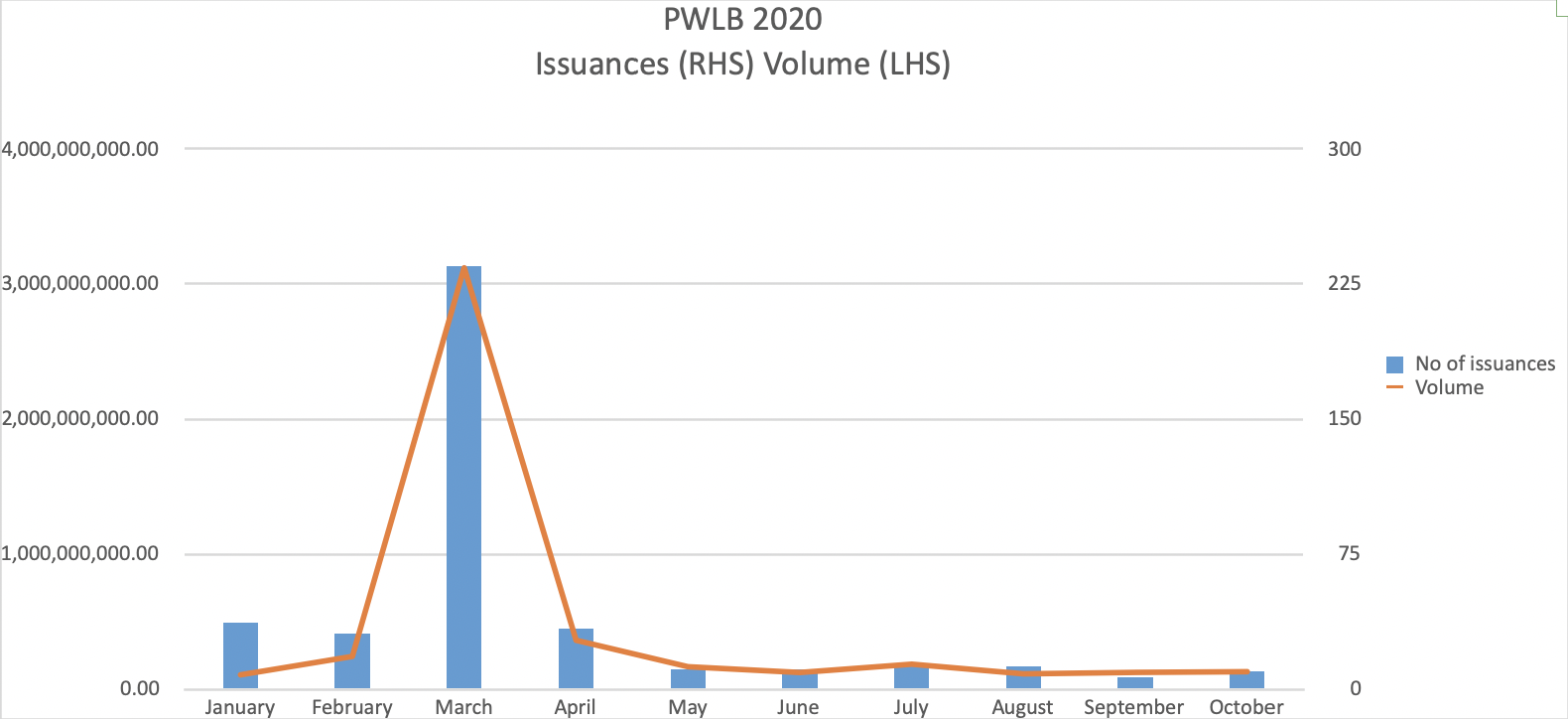

The figures compare to lending from PWLB so far this year of £4.96bn, the bulk of that issued in March.

Divert

But while there is agreement that recent developments mean councils are beginning to turn to bonds, the PWLB decision is likely to recapture the attention of treasury officers.

According to Luke Reeve, a partner in debt advisory at professional services firm EY, the PWLB move is “seismic”. “Borrowing will divert back to the Debt Management Office [PWLB] rather than continue to broaden out to wider markets.” However, Reeve adds that the use of other sources of lending would be “good for responsible financial management and governance”, and would allow markets to price and monitor councils as creditors.

The PWLB rate cut does not come without strings. The Treasury also announced that from now on councils can only borrow from PWLB if finance directors “confirm that there is no intention to buy investment assets primarily for yield” in the three years following a loan. Finance chiefs will also have to submit a plan for capital spending and financing plans, also covering three years.

There is another condition. The restrictions mean PWLB will not lend to a council planning to buy assets for yield “regardless of whether the transaction would notionally be financed from a source other than the PWLB.” Failure to comply with the rules could lead to a council being banned from using the PWLB borrowing facility.

Those clauses could send councils back to the bond market, according to Mike Jensen.

“PWLB now limits what purposes they will lend for, so in order to fund projects that would not comply, then the bond market may remain the appropriate alternative,” he says.

He also suggests that if investors view the PWLB rates as an “upper bound”, and adjust their own spread expectations to below PWLB levels “then activity will pick up again.”

David Blake, startegic director at Arlingclose, sees interest potentially dropping off but points out that with UKMBA bonds trading below Gilts +80bps they still might offer a slim advantage over PWLB. He adds there is also more a little flexibility in structuring a bond over “fairly static” PWLB products. Bonds, he says, are “not completely dead”.

Politics

There was widespread agreement that momentum behind bonds was mounting. Lars Andersson, a Swedish expert on municipal bonds and an early advisor on the UKMBA project, says such agencies have proliferated elsewhere across Scandinavia, the Netherlands and now in France with the Agence France Locale where he is a board member.

“There are many agencies in Europe and typically local authorities use them because they have the best prices in the markets where they exist,” he says. One reason is their lean operating costs, he adds.

And their popularity is borne out by the market share bonds agencies have achieved. The Danish agency has cornered 100% while its Swedish counterpart has around 60%. The French agency is aiming for a 25% share of the local government debt market. Andersson believes agencies should not dominate a market “because you need some competition.”

Prior to this week’s rate change he warned about the PWLB, saying its importance would be undermined “if it continues to make changes for political rather than market reasons,” a comment that may resonate with those wondering why PWLB rates have proved so volatile over the past year.

Aside from cost, there may be other fundamentals that make bonds more attractive in the long term, including the sheer discipline of putting together a bond offering.

“Raising funding from commercial lenders will also bring greater rigour and governance requirements around financial management and credit quality, which should have positive long-term benefits,” says Luke Reeve.

For the time being finance chiefs and treasury officers will be assessing the new borrowing environment. Interest will no doubt swing back to PWLB but bonds are unlikely to be squeezed out entirely.

Photo: HM Treasury, Flickr

Rishi Sunak Photo: HM Treasury, Flickr

FREE monthly newsletters

Subscribe to Room151 Newsletters

Monthly Online Treasury Briefing

Sign up here with a .gov.uk email address

Room151 Webinars

Visit the Room151 channel