A key motive for the original pooling initiative was to attract more institutional commitments to private markets. This appears to have succeeded. While all pools now have made increased commitments to alternatives, the £40bn Border to Coast pool has so far got the most significant private markets tranche.

In May, it reported an additional £3.6bn in commitments to its private market programme including its new UK Opportunities offering and second Climate Opportunities offering, bringing its total private market commitments from partner funds to £16bn. Room151 sat down with deputy CIO Mark Lyon to investigate how this money will be deployed.

In May, it reported an additional £3.6bn in commitments to its private market programme including its new UK Opportunities offering and second Climate Opportunities offering, bringing its total private market commitments from partner funds to £16bn. Room151 sat down with deputy CIO Mark Lyon to investigate how this money will be deployed.

Since your launch six years ago, you have witnessed an exceptional demand for private market strategies among your partner funds. What is driving that trend?

There are probably three key reasons. One is that partner funds have been increasing their allocations to alternatives as the funds mature, they are moving money out of equities and more into private market strategies.

We have got some partner funds who didn’t necessarily have the resources to allocate to private markets pre-pooling and they are now able to access our experienced private markets team to be able to execute their strategies, that was a big draw for some of our partner funds.

Then there is also the recycling of capital through the pool. Some of the partner funds have well-established private markets strategies and as the capital comes back, they are recycling that back through us rather than doing it themselves.

Your latest announcement includes the launch of a new UK Opportunities strategy and a new Climate Opportunities strategy, can you tell us more about these two new strategies?

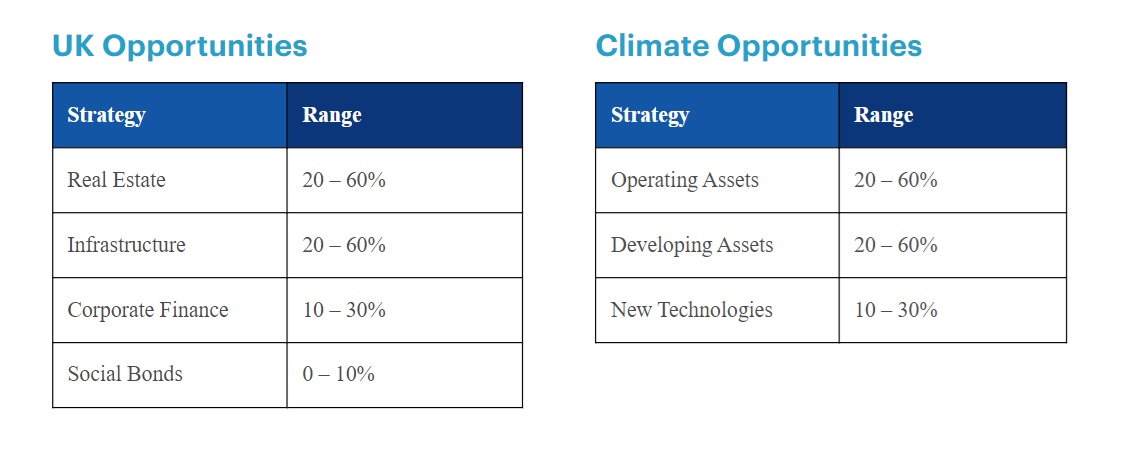

The UK Opportunities strategy is a multi-asset private market strategy across real estate, infrastructure, private equity and private credit. It is a broad private markets strategy focused on additionality, new productive capital, the funding of new companies, where we are really looking for the positive impact.

This is not an impact investment strategy, we are looking for it to have a positive impact, but we are not assessing investment opportunities solely on the scale of their impact, we are very much investment-led, it has to stack up from an investment return perspective. It is UK wide, it is not specific to our partner funds’ regions, we think the best way of deploying capital and getting that diversified exposure is doing it on a UK-wide basis.

As for the Climate Opportunities strategy, we launched the initial offering in 2022 and expected to deploy the capital over three years. However, we were able to deploy it in just short of two years, so we have launched the second iteration of the offering a bit earlier than we thought. We raised £1.4bn in the first offering and received an additional £1.2bn for the second offering which is very much an extension of what we have been doing previously. It is a global strategy which is multi-asset across private equity, infrastructure, private credit and natural capital, things like sustainable agriculture and carbon sequestration. Again, it is very much focused on investment returns, we will measure and report on positive impacts but that is not necessarily how we will determine which investments we select.

What is the risk-return spectrum of these assets, you mentioned the UK Opportunities strategy is focused on additionality, would you describe some of these assets as venture capital?

Yes, some of the strategies in the UK Opportunities strategy are venture and growth capital, university spinouts for example which are very much at the higher end of the risk spectrum, but we are balancing that with lower risk strategies around credit, property regeneration and housing so there is quite a broad risk spectrum across the strategy.

For both UK Opportunities and Climate Opportunities, the target return is 8% per annum, net of all fees and costs. We are not necessarily targeting a barbell approach for UK Opportunities but a mix of lower risk and higher risk strategies with the higher risk strategies accounting for a relatively small part of the overall proposition.

It is the same for the Climate Opportunities strategy. At the moment, our private equity exposure is more growth capital than venture, but venture will form a part of it. We balance off those higher risk assets with some of the lower risk ones, such as private credit, infrastructure and natural capital. We consider our risk profile in terms of operating assets, developing assets and new technologies.

What are the opportunities to invest in the UK specifically, rather than in a global private markets universe?

Because we are doing a broad, multi asset strategy, there are lots of opportunities to choose from. Just to pick out a few of them, we know that there is a huge supply demand imbalance in social- and affordable housing and retirement living is a potentially attractive area for consideration. I think there is also a place for a wider property regeneration exposure where part of it could be housing as part of a much larger regeneration project.

When I think about infrastructure, that includes sectors llike local digital infrastructure, social infrastructure around education or hospitals or transport. When we get into corporate financing, this is the growth and venture capital at the higher end of the risk spectrum, the SME lending at the lower end of the risk spectrum.

I’ve mentioned university spinouts, the UK ranks fourth in the global innovation index, but there is a limited ecosystem to enable these companies to grow at scale. What it is probably lacking is getting those ideas from concept stage to commercial development to growing that business to IPO’ing that business, hopefully in the UK. There is a gap there where we can help to develop that ecosystem further. A lot of that intellectual property coming out of our universities often disappears overseas before it is commercially scalable.

We would also like to do social bonds. That is an investment which has a more explicit link to impact. We are going to be very selective in that space because there are certain bonds where returns may be sacrificed in return for impact. As we are very much investment-led, we are going to make sure that these bonds offer suitable compensation for the risk we are taking. I’d like to do more in social bonds, but it is a relatively small market at the moment, hopefully it will grow over time so that we can deploy more capital.

Do the partner funds invest in a particular asset class (say real estate within UK opportunities) or do they allocate to the entire UK opportunities portfolio?)

No, they allocate to the entire UK Opportunities portfolio which is a multi-asset strategy.

Normally, your partner funds decide on their asset allocation. But within these multi-asset strategies, are you able to adjust the allocation to certain asset classes, for example invest more in credit / real estate etc?

Yes that is correct, for the multi-asset strategies we can adjust the allocation across the different asset classes depending on the relative attractiveness of the opportunity set. Our partner funds determine their asset allocation to the more traditional private market strategies such as private equity or infrastructure, but we also have discretion to tilt these portfolios towards the more attractive sub-sectors. For all of our private market strategies, we agree the risk parameters with partner funds, provide indications of where we expect to invest, and discuss a detailed pipeline so that they get a sense of where the capital is likely to be allocated, but we do have the ability to change that asset allocation when we see the opportunities arise.

—————

FREE bi-weekly newsletters

Subscribe to Room151 Newsletters

Follow us on LinkedIn

Follow us here

Monthly Online Treasury Briefing

Sign up here with a .gov.uk email address

Room151 Webinars

Visit the Room151 channel