The impact of the coronavirus pandemic, lockdown and wider economic uncertainty created deflationary pressures which raise important considerations for the Local Government Pension Scheme writes Daniel Booth.

Since Paul Volcker chaired the US Federal Reserve in the 1980s, we have been experiencing a disinflationary cycle. The impact of the coronavirus pandemic, lockdown and the wider economic uncertainty has created further deflationary pressure, with a rising output gap accompanied by growing unemployment.

This has been combined with longer-term deflationary trends, caused by excessive developed world debt, low levels of labour market bargaining power (due to automation and offshoring) and weak levels of productivity growth.

Authorities internationally have responded to the dire economic situation induced by Covid-19 with a combined economic expansionary response, which may prove to be a critical turning point in the disinflationary cycle.

Stimulation

The extent of both monetary and fiscal stimulation has been larger, faster, and broader than that which followed the 2008 global financial crisis. The monetary stimulus implemented in 2020 saw the balance sheet of the Fed increase significantly with additions including corporate and high yield debt to support credit markets.

Meanwhile, the European Central Bank, alongside other central banks, engaged in rapid quantitative easing programs. The 2020 fiscal stimulus has been extensive and equivalent to four percent of global GDP (versus 1.6% during the 2008 crisis), with government budget deficits reaching the highest levels since the Second World War.

Major differences between the 2020 Covid crisis and 2008 global financial crisis are the impacts on incomes, debt levels and commercial banks.

Commercial banks entered 2008 with excessive leverage multiples (30:1) and minimal capital ratios. Since then, the banks have deleveraged and built up their tier-one capital ratios—a key measure of a bank’s financial strength—so that they reached the current crisis in a healthy position. Consequently, there was little need to offset a reduction in lending. In fact, the opposite has happened, and lending increased. In addition, household incomes have been maintained by government fiscal programs and cash levels have substantially increased.

The quantitative easing we are witnessing currently is a coordinated monetary and fiscal stimulus, with the Treasury borrowing money created by the central bank (‘deficit monetization’).

Rather than ending up as extra central bank reserves this is having a more direct impact on money supply which is expanding at double digit rates. The combination of loose monetary and fiscal policy combined with stable commercial banks and high household and corporate cash levels sets the background for a shift in the inflationary environment.

Also contributing to an inflationary environment is Federal Reserve’s has adoption of an “inflation averaging” target, meaning that to offset any prior inflation shortfall, they will now need to overshoot their inflation target to raise the average.

The Fed recently noted that it would keep rates flat until they have achieved full employment and inflation exceeds their 2% target—so they may be on hold for an extended period.

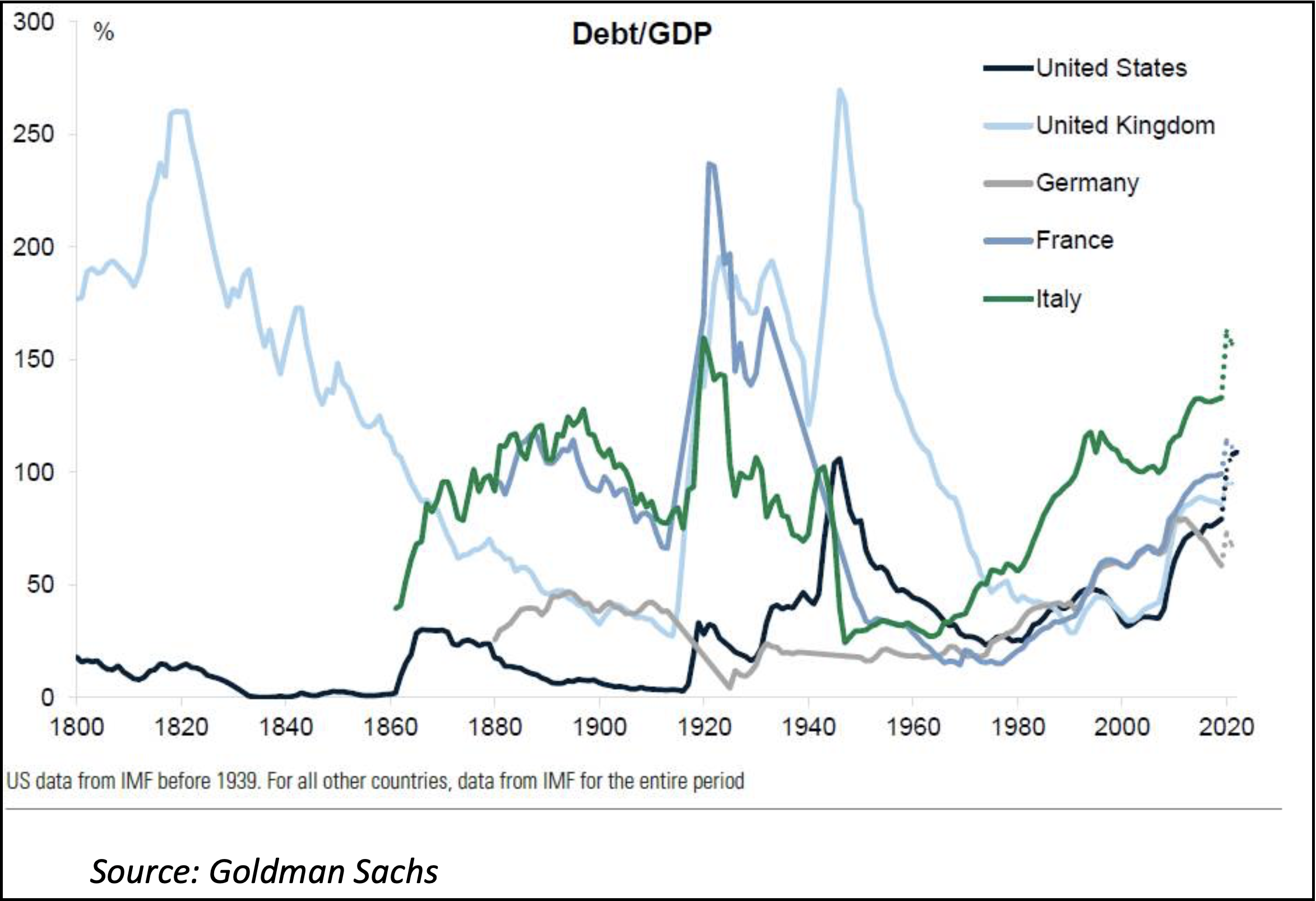

Although central banks cannot lower nominal rates much further due to the zero-bound interest rate, they can lower real rates by increasing inflation and inflation expectations. After 1945, the Fed purchased bonds to keep yields lower than 2-2.5% to keep deficit funding affordable, whilst experiencing 5.5% average inflation (-3% real rate).

This enabled economies to manage down debt burdens after the war. Global debt levels are elevated again, so higher future inflation would help reduce the future real debt burden (see graph below).

Inflation risk

The LGPS should consider the longer-term inflation risk may be under-priced by markets due to the underlying market conditions beginning to change. As discussed above, we are seeing renewed quantitative easing without the offsetting effect of commercial bank deleveraging.

Another factor for the LGPS to ponder is whether we may see a reduction in global supply-side efficiency as we enter a period of de-globalisation (regionalisation) with changing corporate supply chain preferences (onshoring).

This will increase trade frictions and costs, and Brexit in the UK may raise unit labour costs. A study of history also informs us that debt deflations typically turn inflationary, following the path of least resistance, and behaviours may change as participants recognise the new debt perception.

When thinking about impacts on inflation LGPS should note that throughout the coronavirus crisis, households have retained cash levels despite rising unemployment.

Bridgewater estimates current developed world household cash balances are equal to 12.5% of GDP, five times the normal level. It is typical for cash balances to increase during a recession, but the magnitude of the pandemic cash build-up is unique, and any future liquidation of excess cash holdings could act as an additional stimulus.

The authorities are likely to want to stimulate economies further by lowering real interest rates, and with nominal interest rates at the lower 0% bound, they can do this by increasing inflation and inflation expectations.

The Fed’s move to an inflation averaging regime is a clear indication of this direction. In 2021 growth and inflation outlooks are likely to appear higher set against 2020’s low-base impact, combined with ongoing policy stimulation and elevated levels of cash and credit creation as outlined above.

It is clear we’ll see a pick-up in near-term inflation levels, partly due to low base effects from the second quarter of 2020, and it is likely that central banks will tell us this is transitory.

For the LGPS the more important consideration will be the longer-term inflation outcome which will reflect the balance between the impact of the inflationary policies, described above, alongside the residual deflationary forces, such as automation. The LGPS with long-dated inflation linked liabilities should be mindful of the longer-term, inflation risks that has the potential to impact both their assets and their liabilities.

Daniel Booth is chief investment officer at Border to Coast.

Photo by Hakan Nural on Unsplash

AWARDS INFORMATION

Read about the awards here.

Read about the seven categories here.

For submissions click here.

To read case studies of finance team impact, click here.

————————————-

FREE monthly newsletters

Subscribe to Room151 Newsletters

Room151 Linkedin Community

Join here

Monthly Online Treasury Briefing

Sign up here with a .gov.uk email address

Room151 Webinars

Visit the Room151 channel